BNPL has grown fast — but is it still accelerating in 2026, and what does it mean for merchants?

Buy Now Pay Later is no longer an emerging payment solution — it’s becoming infrastructure. After years of rapid adoption, it’s entering a new phase. Growth is still there, but the market is becoming more complex, more regulated, and more competitive.

What began as a checkout novelty is now a strategic battleground. For the major single-lender providers in this space (Affirm, Klarna, PayPal), the ambition is explicit: displace the credit card as the default spending instrument for digital-native consumers.

For merchants, the question is no longer whether to offer BNPL but how to make it work in a changing environment especially as performance gaps between approval, conversion, and real revenue become more visible.

Where BNPL Stands Today: Key Market Figures (Global and U.S.)

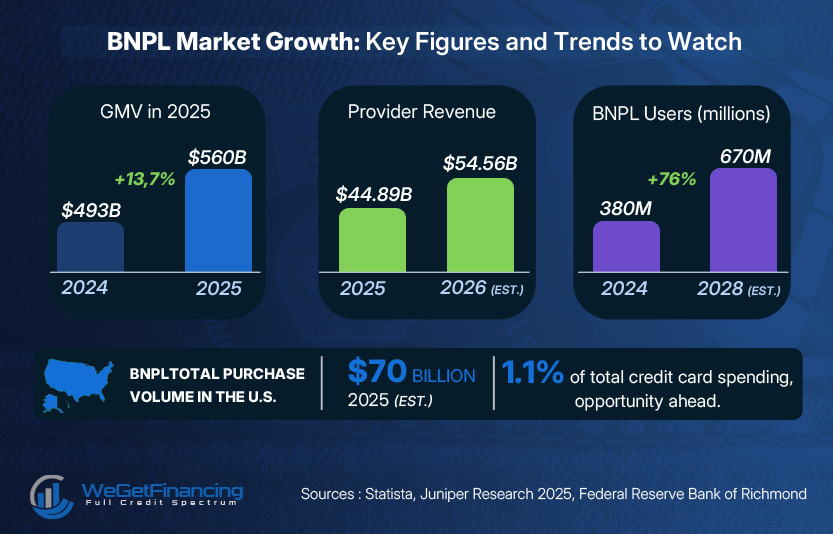

The global BNPL market reached approximately $560 billion in GMV in 2025.

This represents a 13.7% year-over-year increase, with provider revenue estimated at $44.89 billion in 2025 and $54.56 billion in 2026.

Global users reached approximately 380 million in 2024, with projections toward 670 million by 2028.1

BNPL total purchase volume in the US is estimated at roughly $70 billion in 2025.

This represents about 1.1% of total credit card spending — a figure that contextualizes both the opportunity and the distance still to close (Federal Reserve Bank of Richmond — Buy Now, Pay Later: Recent Developments and Implications).

Key Takeaway: BNPL Growth Is No Longer the Full Story

– BNPL is still growing, but at a slower and more complex pace

– Regulation is tightening across all major markets

– Approval rates are becoming a critical performance factor

– Profitability challenges are reshaping the provider landscape

– Merchants need to move from passive BNPL to active optimization

BNPL is no longer about offering financing — it’s about making it work efficiently.

What Is Driving BNPL Growth in 2026

Three structural forces are keeping the engine running.

1. Inflation and purchasing power compression

BNPL is increasingly a cash-flow management tool, not merely a lifestyle convenience.

Persistent cost-of-living pressure has made installment logic appealing beyond younger demographics. Among consumers living paycheck to paycheck, 18% used BNPL in recent months, compared to 9% among those with more financial breathing room.2

2. Gen Z and increasingly, everyone else

42% of Gen Z and 31% of millennials in Europe actively use BNPL services, a behavioral shift we explored in detail in our analysis of how younger consumers are reshaping BNPL adoption. The demographic story is shifting though. In the UK, BNPL usage among adults aged 55–64 more than doubled from 10% in 2023 to 21% in 2024. It’s a strong signal that the product has cleared the generational barrier.

3. E-commerce as the primary channel, in-store as the next frontier

BNPL is becoming a standard feature at checkout across both digital and in-store environments.

The online segment is expected to account for 84.7% of BNPL market share in 2026. In-store BNPL via virtual cards and embedded POS integrations is accelerating, though it remains structurally more complex.

The Challenges Ahead

If growth does not equal health, it does not necessarily mean sustainability either. As BNPL scales, underlying risks, regulatory pressure, and profitability challenges are coming into sharper focus.

The late-payment gap.

Charge-off rates remain relatively low at around 1.8–2%, but approximately 34–41% of users report missing at least one payment. The delta between those two numbers is the real risk indicator. A large population managing liquidity stress without yet tipping into default. One macro shock could move that ratio fast.

At checkout, some customers may accept tighter financing conditions when flexible credit options are limited. But a Buy Now Pay Later purchase does not end at checkout — it becomes a credit journey that must remain frictionless over time.

Regulatory convergence.

The regulatory free ride is over. EU member states were required to transpose the Consumer Credit Directive II (CCD II) into national law by end of 2025, with full enforcement expected across the bloc by Q4 2026. The directive eliminates the short-term interest-free exemption for third-party BNPL providers and mandates creditworthiness assessments.

In the UK, FCA oversight is expected by mid-2026, introducing mandatory affordability checks, credit bureau reporting, and access to the Financial Ombudsman Service.3

In the US, the CFPB withdrew its 2024 interpretive rule, pushing enforcement to state level, a patchwork that creates compliance complexity without reducing overall pressure.

Profitability remains fragile.

For many merchants, Buy Now Pay Later remains one of the most expensive payment methods, with average estimated fees around 2.77%, well above standard credit card rates.

Provider-side economics are equally tight: high credit losses, low consumer fees, and significant marketing spend continue to compress margins. Among BNPL providers — particularly mid-tier and smaller fintech lenders without strong funding or scale — some players might not withstand increasing regulatory and economic pressure.

For merchants, this reinforces the importance of working with diversified financing solutions and ensuring access to multiple lending options, rather than relying on a single provider.

What It Means for Merchants

BNPL is a conversion asset. It is also a cost center. Treating it as only one of the two is a strategic error.

It consistently increases average order value by 20–40% and improves conversion rates by reducing checkout friction. BNPL users spend approximately 6% more than non-BNPL shoppers. Buy Now Pay Later options increase checkout conversion rates by an average of 20–30%. Those numbers justify the merchant discount rate, until they don’t. A practical way to evaluate this is to simulate your own BNPL performance based on your volumes, approval rates, and ticket size.

Approval rates are the hidden variable and one of the most underestimated drivers of financing performance, as we explored in our analysis of BNPL approval gaps and hidden rejection costs. Tighter underwriting under CCD II and equivalent frameworks means more declines at checkout. The regulatory changes could impact conversion advantages, as additional compliance steps lengthen the checkout process. A BNPL integration that converts well today may convert materially worse in 18 months under mandatory affordability checks.

Merchants also need to account for dispute liability, return complexity, and the operational overhead of managing multiple provider integrations. In some retail sectors, BNPL drives 20%+ of sales, making merchants vulnerable to regulatory restrictions or third-party provider issues.

The key to long-term performance is building a flexible and resilient financing strategy — one that balances multiple providers, adapts to customer profiles, and maintains control over approval outcomes.

BNPL Is Becoming More Complex and More Strategic

Single-provider BNPL strategies are becoming a liability. The BNPL category has broadened significantly.

Today’s ecosystem includes everything from short-term pay-in-four products to longer-term installment loans, direct BNPL integrations, and virtual-card solutions that rely on traditional card networks.4 Different providers underwrite differently, approve different customer profiles, and perform differently by market, vertical, and ticket size.

The implication for merchants is structural: a multi-lender approach, running two or three BNPL providers in parallel with intelligent routing, is no longer a premium optimization. It is baseline risk management. Matching the right financing product to the right customer at checkout (based on cart value, geography, approval probability, and cost) is where the real conversion gains live in 2026.

The merchants who will win are not those who simply offer Buy Now Pay Later at checkout. They are those who treat financing as a managed channel with KPIs, provider benchmarking, and a clear view of net revenue per payment method.

BNPL is growing. But the era of passive deployment is over.

FAQ, BNPL Market, Growth & Comparison with Traditional Credit

The global Buy Now, Pay Later (BNPL) market reached approximately $560 billion in gross merchandise value (GMV) in 2025. Growth remains strong, with a projected increase in both transaction volume and provider revenue over the next few years, driven by expanding merchant adoption and consumer demand for flexible payments.

BNPL is growing significantly faster than traditional credit products. While credit card debt in the U.S. exceeds $1 trillion, BNPL represents a smaller but rapidly expanding segment, with double-digit annual growth rates in recent years.

Globally, BNPL users reached around 380 million in 2024 and are expected to grow to approximately 670 million by 2028. This growth is largely driven by younger generations, particularly Millennials and Gen Z, who favor flexible and transparent payment options.

BNPL still represents a relatively small share of total consumer spending. In the U.S., BNPL purchase volume is estimated at around $70 billion in 2025, compared to over $1 trillion in credit card balances. This highlights both the current gap and the significant growth potential of BNPL.

Consumers are increasingly adopting BNPL because it offers better control over budgeting, interest-free installment payments (in many cases), and faster approval processes. BNPL is particularly attractive to younger consumers and those looking to avoid revolving credit debt.

The WeGetFinancing Editorial Team

Expert insights on BNPL, consumer financing, and retention strategies.

Notes

- Chargeflow — Buy Now Pay Later Statistics 2026 (2026). ↩︎

- PYMNTS Intelligence — Pay Later Ecosystem Report (February 2026), via Media Logic analysis. ↩︎

- Checkout.com — BNPL Regulations Across Major Global Markets (2026). ↩︎

- CMSPI / The Paypers — Why Merchants Need a New Approach to BNPL in 2026 (December 2025). ↩︎